🧠🏠The Home Economy Mindset — Why Credit Problems Usually Start at Home? — we discuss practical tools that help households take control of their finances

Most people think credit problems begin with a mistake — a missed payment, a maxed-out card, or an unexpected expense. In reality, credit stress usually starts much earlier and much closer to home.

It starts with how the home economy is organized.

The home economy is the system that connects income, bills, credit, savings, and financial risk. When this system lacks visibility or structure, credit outcomes become unpredictable — even for people who earn good money and try to stay on top of things.

The good news is that control doesn’t come from perfection. It comes from using the right tools in the right order.

🧠 Understanding the Home Economy System

A home economy includes five moving parts:

💵 Income flow (how and when money arrives)

📆 Obligations (bills, subscriptions, debt payments)

💳 Credit usage (cards, loans, limits, balances)

📉 Risk exposure (utilization, missed payments, identity risk)

🔔 Visibility (monitoring, alerts, reviews)

Credit reports respond to patterns created by this system. When one part is misaligned — especially timing or visibility — credit issues tend to follow.

This is why improving credit starts with tools that bring clarity, not quick fixes.

🛠️ Tool 1: The Household Credit Map (Your Foundation Tool)

The Household Credit Map is an important starting point. It provides you with a snapshot of your finances.

Many consumers know they “have a few cards,” but lack a complete picture.

A credit map brings everything into one place:

What it includes

💳 Account name (card or loan)

📊 Credit limit

📉 Typical balance

📆 Statement date

⏰ Due date

🔁 Autopay status

Why it matters

Reveals which accounts drive utilization

Explains why scores fluctuate unexpectedly

Highlights timing conflicts between income and bills

Reduces forgotten or neglected accounts

This tool alone often explains most credit frustration.

📄 Tool 2: Credit Report & Account Overview Tools

Credit reports are not just for disputes or loan applications. Used regularly, they function as a health record for your home economy.

What these tools show

Account status (open, closed, delinquent)

Payment history patterns

Balance-to-limit ratios

Account age and mix

How they support control

Spot issues before they compound

Identify dormant or unnecessary accounts

Confirm payments are reporting correctly

Provide context for future decisions

Reviewing reports isn’t about judgment — it’s about situational awareness.

🔔 Tool 3: Credit Monitoring & Alert Tools

Monitoring tools act as early warning systems. Their purpose is not to generate anxiety, but to shorten response time.

High-value alerts

New account opened

Late payment reported

Balance spikes near limits

Changes to account status

Why they help

Reduce damage duration

Prevent surprises during applications

Catch fraud or errors early

Support proactive adjustments

Used correctly, monitoring tools reduce stress by eliminating the unknown.

📉 Tool 4: Utilization & Balance Tracking Tools

Utilization is one of the most influential — and most controllable — factors in credit outcomes.

Utilization tools track:

📊 Total utilization across all accounts

💳 Individual card utilization

📆 Balance reporting timing

📉 Trend changes over time

Why these tools matter

One high-balance card can outweigh good habits elsewhere

Reported balances often depend on statement dates

Small timing changes can improve outcomes quickly

These tools turn utilization from a mystery into a manageable variable.

📆 Tool 5: Bill Calendars & Cash-Flow Planners

Many credit issues are timing problems, not affordability problems.

Cash-flow tools show:

When income arrives

When bills are due

Where gaps exist

How credit fills those gaps

What a bill calendar provides

Visibility into clustered due dates

Opportunities to align bills with paydays

Early warning for tight months

Reduced reliance on credit for timing gaps

When cash flow becomes predictable, credit stabilizes naturally.

🧮 Tool 6: Calculators & Scenario Tools

Financial calculators don’t make decisions — they remove guesswork.

Useful tools include:

Utilization impact calculators

Paydown modeling tools

Payment timing scenarios

Balance transfer estimators

Why they help

Show consequences before action

Reduce emotional decision-making

Support planning instead of reacting

Build confidence through clarity

These tools transform uncertainty into informed choice.

🛡️ Tool 7: Identity & Risk Protection Tools

Identity protection tools don’t prevent all problems — they reduce exposure and recovery time.

They help by:

Alerting you to compromised data

Monitoring dark web activity

Supporting faster response to fraud

Protecting long-term credit history

In the home economy, these tools act like insurance — quiet until needed, critical when they are.

🧠 Tool 8: Education & Context Tools

Understanding why things happen is as important as seeing what happens.

Education tools provide:

Explanations of credit behavior

Context for score movement

Guidance on timing and risk

Confidence to act deliberately

Households with context make calmer, more consistent decisions.

🔁 How These Tools Work Together

No single tool fixes credit. Control comes from layering tools:

🛠️ Credit Map → clarity

📄 Reports → accuracy

🔔 Monitoring → awareness

📉 Utilization tools → control

📆 Cash-flow tools → stability

🧮 Calculators → confidence

🛡️ Protection → resilience

🧠 Education → consistency

This is the home economy system in action.

✅ Final Takeaway

🧠 Credit problems usually start at home — not because people fail, but because systems lack visibility.

With the right tools:

Credit becomes predictable

Stress decreases

Decisions improve

Outcomes follow naturally

This foundation makes everything else in the series possible. Next, we explore how to monitor credit without creating stress or obsession.

YourCreditInsights can help you with the tools you need to take more effective control of your finances.

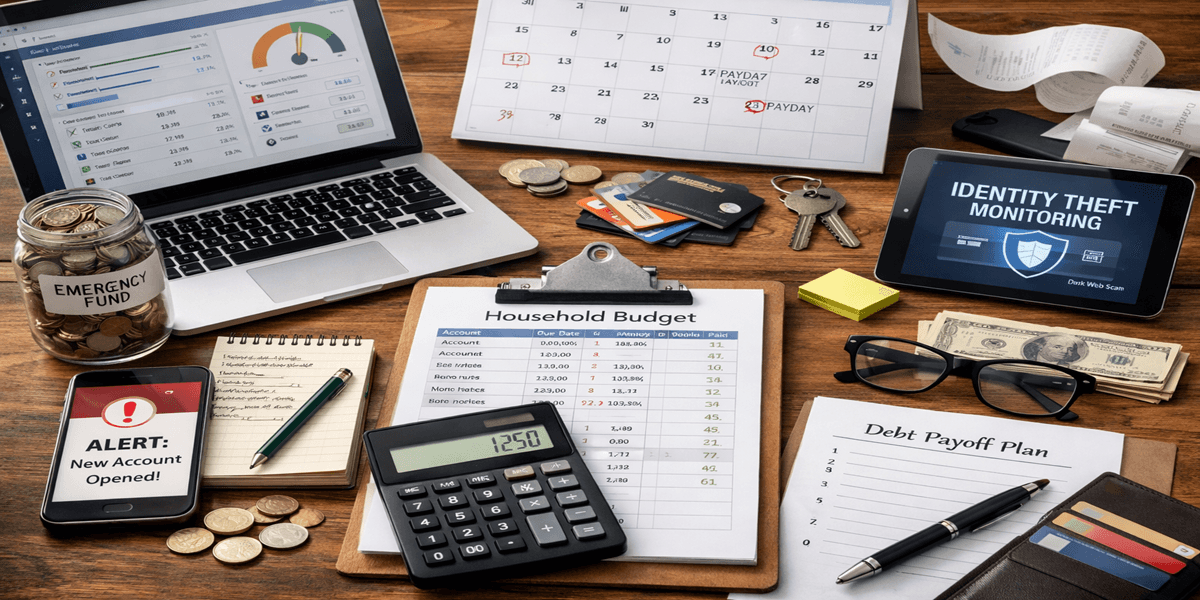

🛠️ Household Credit Map → Dashboard snapshot

📄 Credit Overview → Full report access

🔔 Monitoring → Alerts & notifications

📉 Utilization → Balance meters

📆 Cash-flow tools → Bill calendar

🧮 Calculators → Scenario modeling

🛡️ Protection → Identity monitoring

🧠 Education → Guided insights