❄️The Debt Snowball Method: How It Works, Pros & Cons, and Whether It’s Right for You💳

Debt can feel overwhelming — especially when you’re juggling multiple balances, different interest rates, and minimum payments that barely seem to make a dent. If you’ve been looking for a clear, structured way to tackle what you owe, you may have come across the debt snowball method.

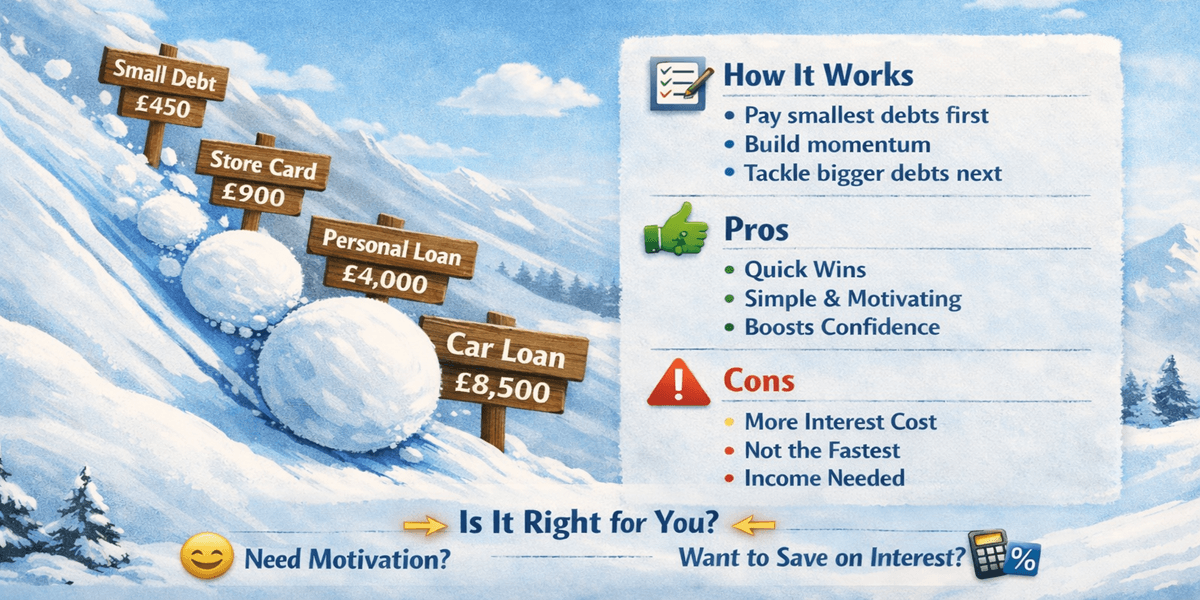

The debt snowball method involves paying off your smallest debts first, regardless of interest rate, so you can build momentum and confidence before tackling larger balances.

In this guide, we’ll explain:

✅ How the debt snowball works

📊 Step-by-step instructions

👍 The main advantages

⚠️ The potential drawbacks

🤔 How to decide if it’s right for you

🔁 How the Debt Snowball Method Works

The idea behind the debt snowball is simple: quick wins build motivation.

Instead of focusing on interest rates, you focus on balance size.

Step-by-Step Process

List all your debts from smallest balance to largest.

Make minimum payments on all debts.

Put any extra money toward the smallest balance.

Once the smallest debt is paid off, ➜ roll that full payment amount into the next smallest debt.

Repeat until all debts are cleared.

Each time you eliminate a debt, the amount you can put toward the next one grows — like a snowball rolling downhill.

📋 Example of the Debt Snowball in Action

Let’s say you have:

Credit Card A: £450

Store Card: £900

Personal Loan: £4,000

Car Loan: £8,500

Using the debt snowball:

You focus all extra money on the £450 credit card first.

Once cleared, you apply that payment toward the £900 store card.

Then move to the £4,000 loan.

Finally, attack the £8,500 balance.

By the time you reach the larger debts, you’re throwing much bigger monthly amounts at them.

👍 Pros of the Debt Snowball Method

1️⃣ Psychological Motivation

Paying off a debt quickly creates a sense of achievement. That motivation can be powerful — especially if you’ve struggled to stick to repayment plans in the past.

Small wins reinforce good financial habits.

2️⃣ Simplicity

The system is easy to follow. You don’t need complex spreadsheets or interest calculations. You simply focus on the smallest balance.

For people who feel overwhelmed by numbers, simplicity matters.

3️⃣ Builds Financial Discipline

Because you see visible progress early on, you’re more likely to stay consistent. Consistency is often more important than mathematical perfection.

4️⃣ Reduces Mental Load

Each paid-off debt is one fewer statement, one fewer due date, and one fewer source of stress.

That clarity can improve your overall financial confidence.

⚠️ Cons of the Debt Snowball Method

1️⃣ You May Pay More Interest

The biggest criticism of the debt snowball is that it ignores interest rates.

If your smallest debt has a low interest rate, but a larger debt has a very high one, you could end up paying more overall by delaying repayment of the expensive balance.

2️⃣ Not the Fastest Financial Strategy

Mathematically, the debt avalanche method — which prioritises highest interest rates first — will usually save more money in the long run.

The snowball prioritises psychology over optimisation.

3️⃣ Requires Steady Income

Like any repayment strategy, the snowball works best when you can consistently put extra money toward your balances.

If income is unpredictable, progress may stall.

❄️ Debt Snowball vs Debt Avalanche

Here’s a quick comparison:

Debt Snowball | Debt Avalanche |

Focuses on smallest balance first | Focuses on highest interest rate first |

Builds motivation quickly | Saves more money long term |

Behaviour-focused | Maths-focused |

Easier for beginners | Better for maximising efficiency |

If you struggle with consistency, the snowball’s psychological boost can be worth more than interest savings.

If you’re disciplined and numbers-driven, avalanche may suit you better.

🧠 Why the Snowball Works for Many People

Personal finance is behavioural.

Research and experience consistently show that people don’t fail at debt repayment because they lack knowledge — they fail because they lose momentum.

The snowball method reduces the emotional weight of debt.

When you see accounts disappearing, your confidence grows. That confidence often leads to better budgeting decisions, fewer impulse purchases, and stronger long-term habits.

📌 When the Debt Snowball Might Be Right for You

The debt snowball may be a good fit if:

You feel overwhelmed by multiple debts

You’ve started repayment plans before but quit

You need quick visible progress

Your interest rates are relatively similar

Motivation is your biggest challenge

🚫 When It Might Not Be Ideal

You may want to reconsider if:

One debt has a significantly higher interest rate

You’re focused on minimising total repayment cost

You’re comfortable with structured financial calculations

You have strong discipline already

In these cases, the avalanche method may be more efficient.

💡 Tips to Make the Debt Snowball Work Even Better

If you choose the snowball method, strengthen it with these steps:

✔️ Build a Small Emergency Fund First

Even £500–£1,000 can prevent new debt if unexpected expenses arise.

✔️ Automate Minimum Payments

Avoid missed payments and credit score damage.

✔️ Track Progress Visually

Use a chart, spreadsheet, or whiteboard to see balances shrinking.

✔️ Avoid Taking On New Debt

The snowball only works if the total amount owed is decreasing.

📊 Does the Debt Snowball Help Your Credit Score?

Indirectly — yes.

As balances decrease:

Credit utilisation improves

Fewer accounts remain open

Payment consistency strengthens your profile

However, closing older accounts may impact average credit age. If improving your credit score is a key goal, you may want to think carefully about which accounts to close.

🏁 Final Thoughts: Is the Debt Snowball Worth It?

The debt snowball method isn’t mathematically perfect — but it’s powerful.

For many people, behaviour beats optimisation.

If small wins will keep you consistent, motivated, and moving forward, the snowball method can be an effective way to regain control.

The best debt strategy isn’t the one that looks smartest on paper.

It’s the one you’ll stick with.