⚖️Less Is More — How Fewer Credit Moves Can Improve Your Score Faster📈

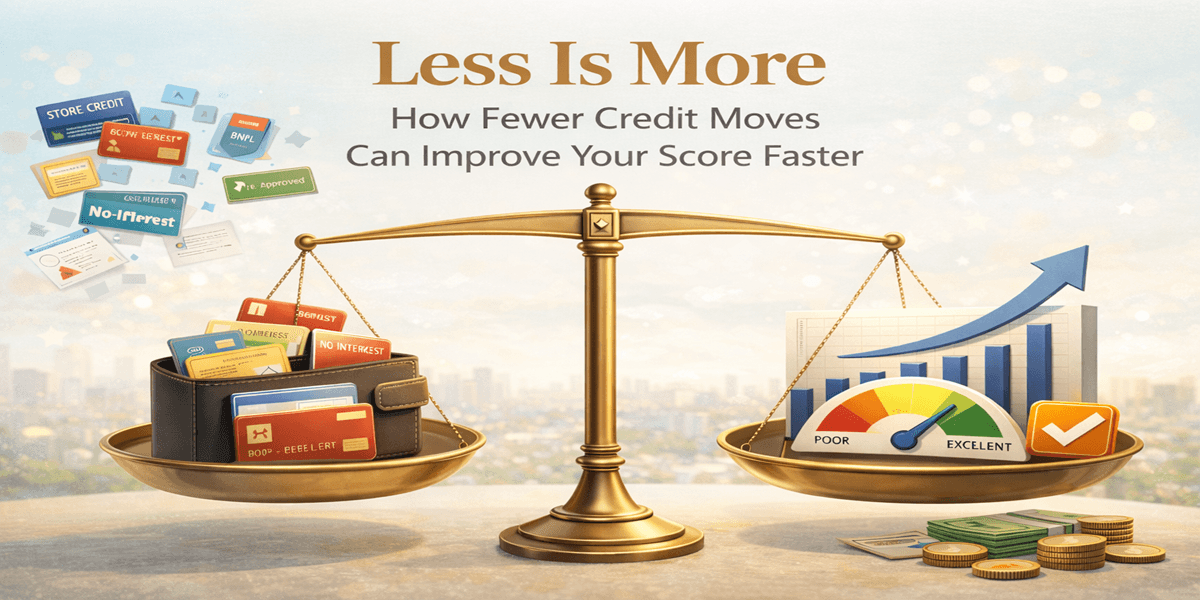

When consumers commit to improving their credit, the instinct is often to act quickly. Apply for a new card. Transfer balances. Open a store account for a discount. But in credit management, more activity doesn’t always mean more progress.

In fact, restraint is often your most powerful tool.

Why Too Much Activity Can Hurt

Most credit applications result in a hard inquiry being added to a consumer’s credit report. In some cases, a soft inquiry may be used, which does not affect the consumer’s credit score. Consumers are generally notified of the type of inquiry that will be conducted before an application is finalized and should review this information carefully before providing consent. While a single hard inquiry typically has a limited impact on a credit score, multiple hard inquiries within a short period of time may be considered by lenders when assessing overall credit risk.

From a lender’s perspective, frequent changes raise questions:

Why is this borrower seeking so much new credit?

Are they under financial pressure?

Is risk increasing?

Credit scores are designed to reflect stability, not speed.

The Power of Focusing on One Card

Instead of juggling multiple balances, choose one primary card:

Use it for regular spending

Keep utilization below 30% (ideally under 10%)

Pay it down consistently

This creates a clear, positive usage pattern that scoring models recognize.

Meanwhile, keep other cards open but unused or lightly used to maintain available credit.

Why Q1 Is the Best Time to Pause Applications

The first quarter of the year is ideal for consolidation:

Holiday balances are still settling

Income patterns stabilize

Spending habits reset

Avoid:

Store cards

Buy-Now-Pay-Later plans

Promotional financing offers

Even “no-interest” deals can add complexity and reporting noise.

Check Autopay—Don’t Assume It’s Working

January is one of the most common months for missed payments due to:

Changed due dates

Insufficient funds after holiday spending

Expired cards linked to autopay

Take ten minutes to confirm:

Payment amounts

Linked bank accounts

Statement closing dates

One missed payment can undo months of positive behavior.

Why Simplicity Improves Scores

Credit scoring systems reward:

Repeated on-time payments

Gradual balance reductions

Minimal volatility

Boring credit behavior is good credit behavior.

Less activity means clearer data—and clearer data builds lender confidence.

Avoid “Credit Curiosity” Traps

Checking offers or pre-approvals can feel harmless, but converting them into applications without need adds risk.

Before applying, ask:

Does this support my annual goal?

Will it improve my utilization?

Can I manage another account responsibly?

If the answer isn’t clearly “yes,” wait.

Progress Without Pressure

Credit improvement isn’t a race. It’s a system. Slow, controlled movement often delivers faster long-term results than constant change.

This year, let discipline outperform impulse.